Executor Checklist UK 2026: Step-by-Step Estate Guide

Executor’s Checklist 2026: Step-by-Step Guide to Administering an Estate

Being named as an executor is an important responsibility. At a time when you may be dealing with grief, you are also expected to manage legal, financial and administrative tasks correctly. Many people feel unsure where to begin, especially if they have never dealt with probate or estate administration before.

The role can feel overwhelming at first, but it becomes far more manageable when broken down into clear steps. Understanding what is required at each stage will help you stay organised and avoid costly mistakes.

This executor’s checklist for 2026 explains the full process in a structured way. It will help you understand your duties, reduce risk and administer the estate with confidence.

What Does an Executor Do?

An executor is responsible for managing a person’s estate after they pass away. This includes identifying and collecting assets, settling any debts or liabilities, and distributing what remains to the beneficiaries named in the will.

The role is both practical and legal in nature. Executors must deal with financial institutions, government bodies and sometimes property transactions. At the same time, they must ensure that everything is carried out in accordance with the law and the wishes set out in the will.

It is important to understand that this role carries legal responsibility. If mistakes are made, such as distributing assets too early or failing to settle debts, an executor can be held personally liable. This is why careful record keeping and a structured approach are essential throughout the process.

Step 1: Register the Death

The first step is to officially register the death. In England and Wales this must usually be done within five days, unless there are exceptional circumstances.

You will need the medical certificate provided by a doctor or hospital. Once the death is registered, you will receive an official death certificate. It is advisable to request multiple copies at this stage, as banks, insurers and other organisations will often require original documents before releasing information or funds.

Registering the death also allows you to begin notifying relevant authorities and organisations, which is a key part of the early administration process.

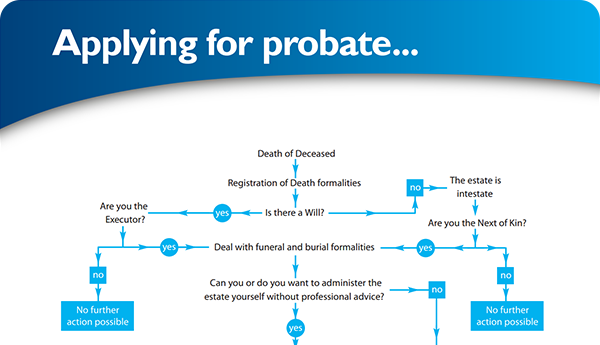

Step 2: Locate the Will

The next step is to locate the will. This document confirms who has been appointed as executor and provides instructions for how the estate should be distributed.

The will may be stored in several places, including the deceased’s home, with a solicitor, or held securely by a bank. If you are unsure where it is, you may need to make enquiries with professionals who may have assisted the deceased during their lifetime.

If no valid will can be found, the estate will be administered under intestacy rules. These rules set out a fixed order of inheritance, which may not reflect the deceased’s personal wishes. This can also make the administration process more complex.

Step 3: Secure the Estate

Before taking any further steps, it is essential to secure the estate. Executors have a duty to protect the assets and preserve their value until they are distributed.

If the deceased owned property, you should ensure that it is locked, insured and regularly checked. Insurance providers should be informed, as standard policies may not remain valid once a property becomes unoccupied.

Valuable items such as jewellery, documents and personal possessions should also be safeguarded. Taking these steps early reduces the risk of loss, damage or disputes later in the process.

Step 4: Notify Relevant Organisations

You will need to inform a range of organisations about the death. This includes banks, building societies, utility providers, insurers and government departments.

Notifying these organisations ensures that accounts are frozen where necessary and prevents further charges or misuse. It also allows you to begin gathering information about the estate’s assets and liabilities.

Many people use the Tell Us Once service, which can notify several government departments in one step. However, you will still need to contact private organisations separately, and each may have its own requirements for documentation.

Step 5: Value the Estate

Before probate can be applied for, you must calculate the total value of the estate. This is a critical step, as it determines whether inheritance tax is due and affects how the estate is administered.

The valuation should include all assets, such as property, savings, investments and personal belongings. At the same time, you must identify any debts, including mortgages, loans and outstanding bills.

Accuracy is very important. Undervaluing the estate can lead to penalties, while overvaluing it may result in unnecessary tax payments.

Step 6: Check if Probate Is Required

Not every estate requires probate. In smaller or simpler estates, assets may be released without the need for a formal grant.

However, probate is usually required where property is involved or where financial institutions require formal authority before releasing funds.

Step 7: Apply for Probate

If probate is required, you will need to submit an application to the Probate Registry. This involves completing the appropriate forms, submitting the will and providing details of the estate’s value.

Once the application has been processed and approved, you will receive a Grant of Probate, giving you legal authority to administer the estate.

Step 8: Deal with Inheritance Tax

Inheritance tax may need to be paid before probate is granted. The amount depends on the value of the estate and any available reliefs.

Tax is usually payable within six months of the date of death, and delays can result in interest or penalties.

Step 9: Collect the Assets

Once probate has been granted, you can begin collecting the estate’s assets. This may include closing accounts, selling property and transferring funds into an executor’s account.

Keeping clear financial records at this stage is essential for transparency and accountability.

Step 10: Pay Debts and Expenses

Before distributing any inheritance, all debts and expenses must be settled, including funeral costs and outstanding liabilities.

If debts are missed, the executor may be personally responsible for repayment.

Step 11: Distribute the Estate

Once all debts have been paid, you can distribute the remaining assets according to the will.

Clear communication and accurate record keeping help prevent disputes.

Step 12: Finalise the Estate

The final step is to prepare estate accounts showing all income, expenses and distributions.

Once approved by beneficiaries, the estate can be formally closed.

Common Mistakes Executors Should Avoid

Common mistakes include distributing assets too early, inaccurate valuations and poor record keeping.

How Long Does It Take to Administer an Estate?

A straightforward estate typically takes six to twelve months, but complex cases can take longer.

Do You Need Professional Help?

Many executors choose professional support to reduce risk and ensure compliance throughout the process.

Final Thoughts

Acting as an executor becomes manageable when broken into structured steps. Following this checklist helps ensure the estate is administered correctly and efficiently.

Back To BlogShare This Post

Recent posts

- What Are the Duties of an Executor? By , 15/06/2026

- Executor vs Administrator UK: What’s the Difference? By , 15/06/2026

- Executor Liability: Can You Be Held Personally Liable? By , 15/06/2026

2015 Archive

2016 Archive

2018 Archive

2019 Archive

2020 Archive

2023 Archive

- July 10 posts

0 Archive

- December 1 posts

Blog Categories

Find your way through the probate maze

Click here to follow our step-by–step probate process guide

Testimonials

Excellent service, everything went very smoothly. Like to thank Ann and her team.... read more

Good & Reliable service, always kept up to date with what was happening. Value for money.... read more

Latest Tweet

Follow @ProbateBureau

Contact Us

0800 028 2837 info@probatebureau.comTHE PROBATE BUREAU

3 Crane Mead Business Park

Crane Mead

Ware

Hertfordshire

SG12 9PZ

×